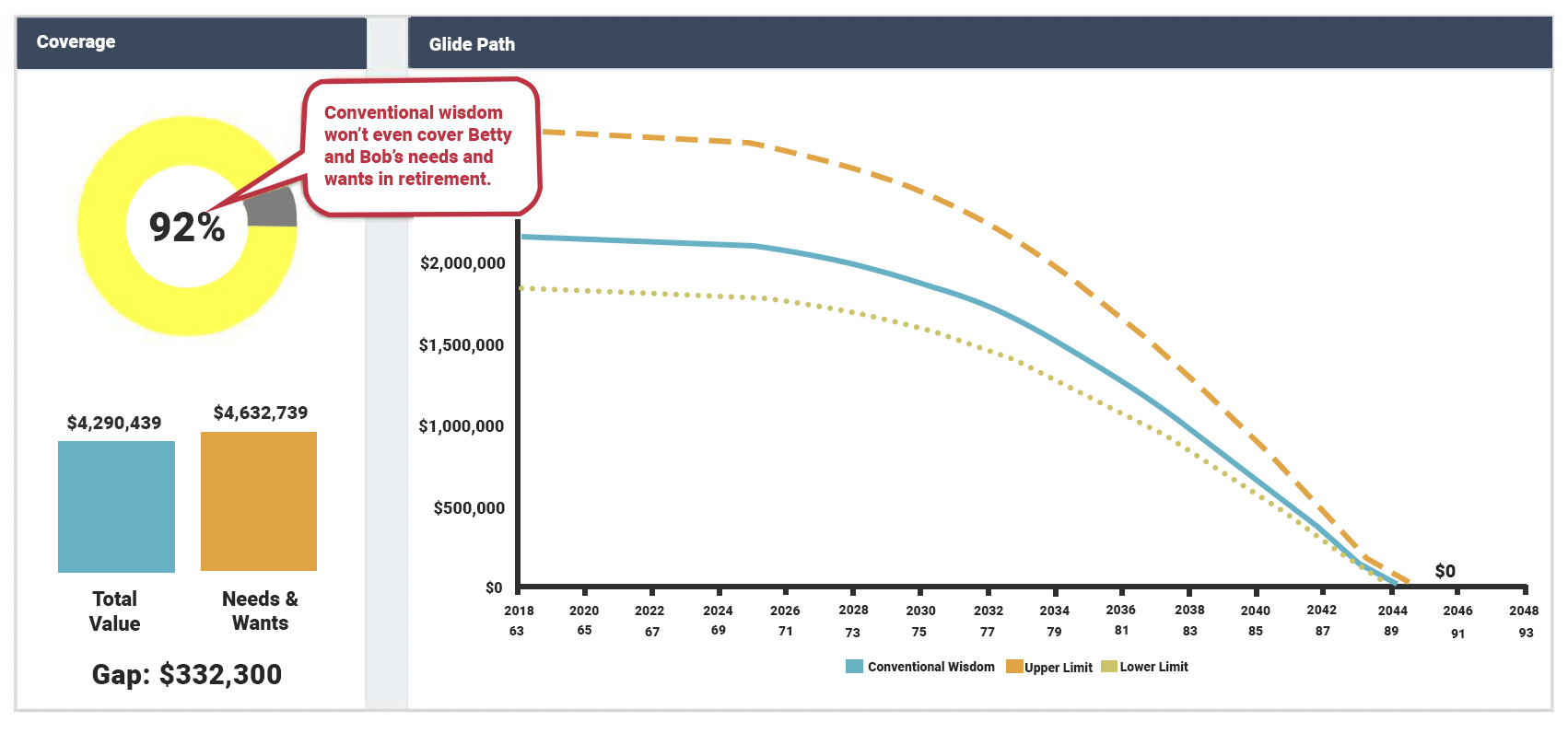

They learned that spending their retirement assets in the typical “conventional wisdom” order – spending all of the taxable, then tax-deferred, and then tax-exempt accounts – won’t actually meet all of their income needs in retirement! There was a large income shortfall and their portfolio would run out of money before Betty would expect to pass away.

They learned that spending their retirement assets in the typical “conventional wisdom” order – spending all of the taxable, then tax-deferred, and then tax-exempt accounts – won’t actually meet all of their income needs in retirement! There was a large income shortfall and their portfolio would run out of money before Betty would expect to pass away.

Betty and Bob notice in our meeting a strategy called ‘Opposite of Conventional Wisdom’, which means spending down their savings in the exact opposite order from Conventional Wisdom: First tax-exempt, then tax-deferred, and then taxable. Guess what? Opposite of conventional wisdom meant more money for Bob & Betty and would provide for Betty throughout her lifetime as well.

Just to be sure there were no better strategies, we analyzed several other potential strategies.

Just to be sure there were no better strategies, we analyzed several other potential strategies.

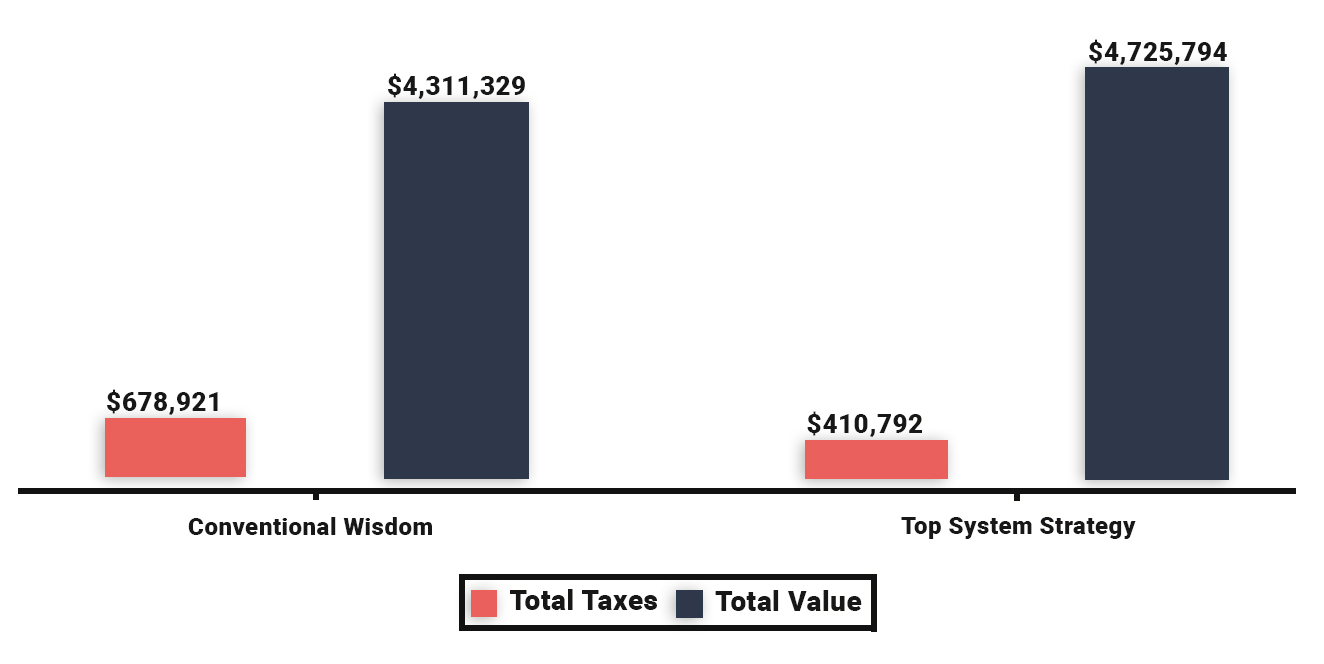

Betty and Bob were surprised to see that there were many strategies that were better than conventional and opposite conventional wisdom! The best strategy actually provided for an additional $414,465 for the couple over the conventional wisdom strategy recommended to them by their original advisor. This was accomplished by managing taxes and coordinating their Social Security claiming strategy.

The recommended top withdrawal strategy prescribed taking advantage of partial Roth conversions each year to minimize the total taxes owed over their retirement horizon. This also allowed them to reduce their Required Minimum Distributions (RMDs) and ultimately save on Social Security taxes as well. As you can see by the graph above, the difference in taxes with the top strategy over conventional wisdom is $268,129 by using partial Roth conversions strategically.